Credit Score: How Does It Affect Your Car Payment?

Let’s start by asking what exactly is credit?

What is credit?

The definition according to Experian, one of the credit bureaus is, “Credit is borrowed money that you can use to purchase goods and services when you need them. You get credit from a credit grantor, whom you agree to pay back the amount you spent, plus applicable finance charges, at an agreed-upon time.”

What is a credit score?

Ok. So now we know what credit is. What about a score? A piece of music it is not. How would you feel if a random stranger on the street asked to borrow a large sum of money and promised to pay it back? You might be a little hesitant. You have no proof that this person is ever going to pay back. How do you know if they will make payments, or even make them on time? Do they have a job, can they prove it? have they borrowed money before and paid it back? Did they pay it all back early?

These are the stats you’d like to know right?

Well, this is kind of the same as how a bank or auto loan company look at it too. It’s a little more sophisticated in this modern age, though. Payment records, inquiries, amounts owed, length of credit history, new credit accounts, and types of credit used, are all factors in deciding a risk-based calculation on how likely you are to pay them back. The following diagram shows how these factors count towards calculating the score.

This calculation produces a number which determines your credit score. Credit scores typically change monthly as account information gets recorded/reported. Your personal credit score will range from 300-850.

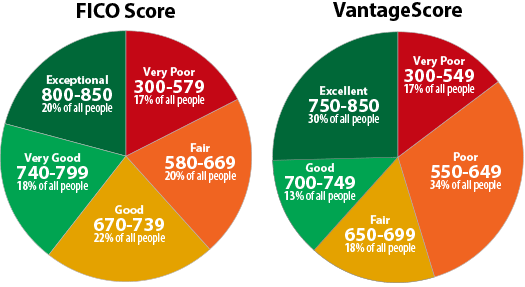

What is a good score?

Why does your score matter?

Sometimes, it isn’t exactly straightforward and there are exceptions, but in essence, the better the score you have, the more likely you are to get a loan and the more likely you are to get a better interest rate, which in turn will reduce your payment. A history of missed payments will reduce your score, therefore, increasing your risk to lending institutions and increasing the interest rates on loan approvals.

Missed payments as you can see from the pie chart above are pretty heavily weighted, so avoiding this will definitely help keep your credit score in good standing. Lots of missed payments may make the risk too high for any lending institutions in which case, you may not be approved at all. This can also be the case if there already too much money that is still owed vs monthly income.

Recent Comments